The following is part of Greenberg Traurig’s ongoing series analyzing cross-border data transfers in light of the new Standard Contractual Clauses approved by the European Commission in June 2021.

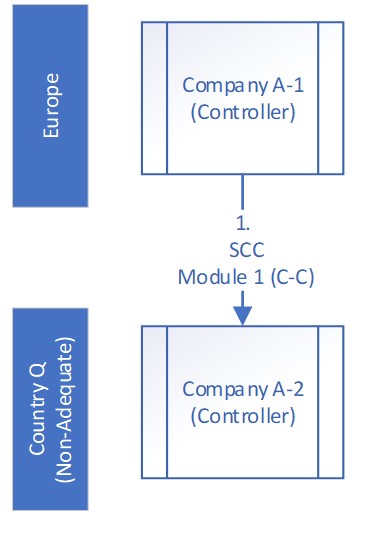

Controller A-1 (EEA) → Controller A-2 (Non-EEA)

| Visual | Description and Implications |

|

|